Capital: Debited or Credited — Understanding the Accounting Truth Behind Owner’s Equity

Capital: Debited or Credited — Understanding the Accounting Truth Behind Owner’s Equity

The question of whether capital is debited or credited lies at the heart of fundamental accounting practice, shaping how businesses track and report their financial health. In the dynamic world of financial reporting, an accurate understanding of this accounting principle ensures transparency, compliance, and informed decision-making. Contrary to intuitive confusion, capital resides within the balance sheet’s owner’s equity section and, by definition, must be recorded using standard double-entry logic—making its status clear but often misunderstood.

Capital as an Owner’s Equity Account Capital, in accounting, represents the residual interest in a business after liabilities are deducted from total assets. Despite its critical role, it is classified as an equity account—not a revenue or expense—meaning its normal balance is credit. When owners invest capital into a business, this infusion increases the capital account, entering the transaction via a credit.

This reflects the fundamental principle that increases in equity (especially by capital contributions) debit the accounting equation from the asset side and credit the equity side. According to the basic accounting equation: Assets = Liabilities + Equity; capital, as a component of equity, must maintain a credit balance. This is not a mere convention—it is a foundational rule—ensuring that every capital infusion is properly documented to reflect true ownership stakes.

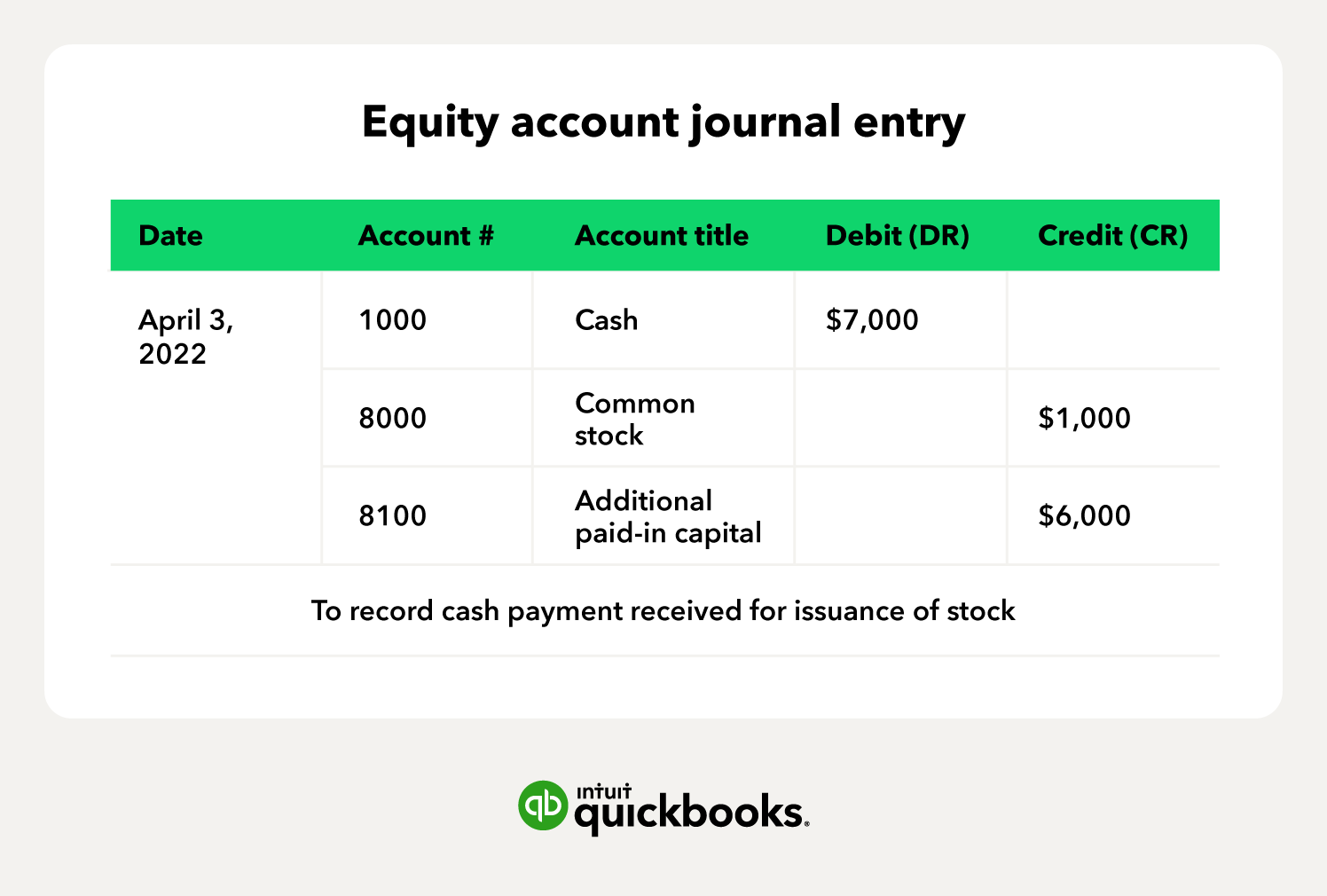

When capital is initially contributed, whether through cash, property, or services, the transaction manifests as a credit to the capital account and a corresponding debit to a liability (such as “Capital — Cash” or “Capital — Revaluation”), though the latter two are less common in straightforward investments. This dual entry preserves the balance, satisfying the accounting equation’s integrity. For example, if a founder deposits $50,000 in cash, the journal entry reads:

```plaintext Debit: Capital Account – $50,000 Credit: Cash — Capital Contributions ``` Debit vs.Credit: Why Capital Isn’t Like Liabilities or Equity Transactions

While liabilities also carry credit balances, capital operates separately. Unlike debts that increase obligations, capital injections strengthen ownership. Journal entries consistently treat capital as credit to ensure clarity.As financial expert Robert Kiyosaki noted, “The way you record your finances determines how you see your success.” This principle underscores the necessity of crediting capital

Related Post

Call of Duty Mobile Season 10 Breakdown: What the Latest Campaign Reveals About Tactical Evolution and Mobile Excellence

Bebe Winans’ Current Wife: A Union Rooted in Faith, Family, and Resilience

Unveiling Mariah Brown’s Wedding Insights and Discoveries: A Deep Dive into Love, Ritual, and Modern Tradition

Gloria Delouise Cause of Death: Unraveling the Tragic End of a Life Lived in Shadow